Summary

- AI likely represents one of the most consequential technological shifts in human history.

- Technological revolutions rarely unfold in a straight line. Instead, they are overestimated in the short run and underestimated in the long run.

- AI will create dramatic divergence between businesses that can adapt and businesses that get left behind.

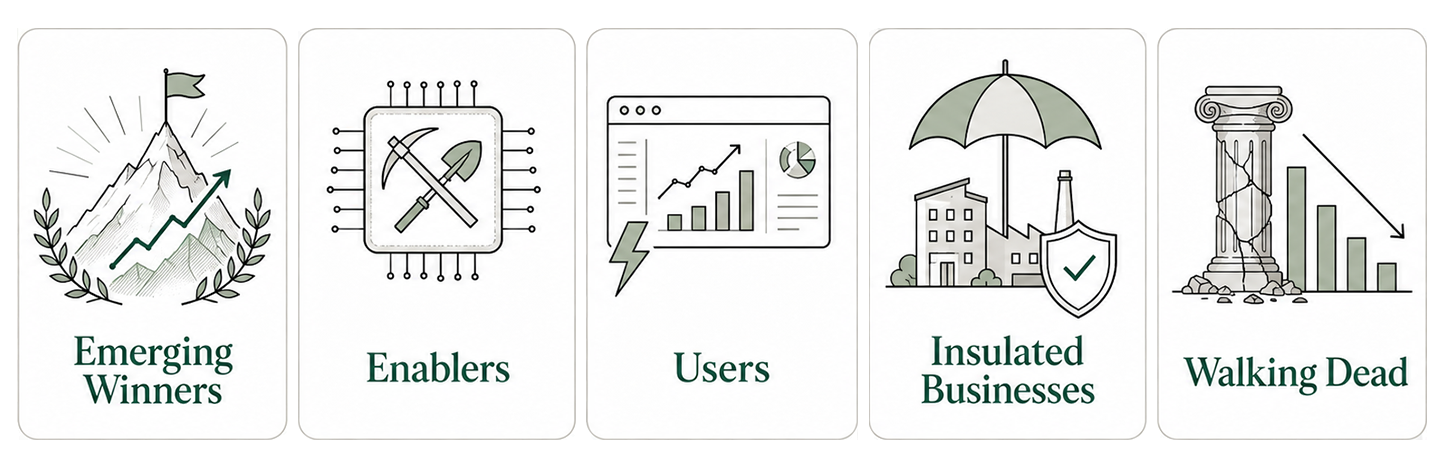

- Companies will fall into five categories: Emerging Winners, Enablers, Users, Insulated Businesses, and the Walking Dead.

- During this period of massive economic and technological disruption, investors should be wary of passive and momentum-based strategies—which may be disadvantaged during this time of transition.

- Flexible investors applying bottom-up fundamental research, careful stock selection and a rigorous valuation discipline that incorporates the implications of AI will be best-positioned to navigate change in this era.

Introduction

While past periods of technological acceleration, including the print and maritime era (1500–1750), the scientific revolution (1550–1800), the first and second industrial revolutions (1760–1840 and 1870–1914), the atomic and electronic age (1945–1970), and the digital and internet era (1980–2020) provide useful context, the advent of artificial intelligence (AI)1 represents a unique moment in human history that will profoundly transform the political, social, economic and investment landscape.

The rate of this transformation will be neither as fast as the promoters promise nor as slow as the deniers would wish. Instead, like all other revolutionary technologies, it will follow the wave of Amara’s law which states that, “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

While we are still in the overestimating/hype phase of Amara’s cycle, our research indicates that the deployment of AI is already accelerating the growth of select, well-positioned and nimble companies by both increasing their competitive advantages and reducing their costs. At the same time, we see an increasing number of once bullet-proof businesses whose competitive advantages and growth prospects are being gradually but relentlessly undermined.

With this investment backdrop, the wheels are beginning to come off many widely accepted but inflexible portfolio strategies, most notably those that are passive, overly diversified, illiquid or reliant on past patterns (such as dividend history), and those that forsake price discipline. In significant transitions, strategies optimized to the past rarely succeed.

Instead, we see the AI transformation rewarding active, adaptable portfolio managers that use fundamental research, careful stock selection and a valuation discipline, and consequently believe investors may be wise to allocate a larger portion of their portfolios away from richly valued indexes and illiquid strategies towards thoughtful, active management.

Investment Philosophy

A research-driven framework to identify AI’s emerging winners—and avoid the casualties

At Davis Advisors, our investment discipline rests on fundamental research that evaluates the durability, quality and long-term prospects of each portfolio investment. This assessment includes a lens focused on the threats and opportunities created by AI, and groups each potential investment into one of five categories: the emerging winners, the enablers, the users, the insulated and the walking dead. Understanding these categories can help investors navigate increasingly volatile conditions.

Economic Framework

AI is likely to become a widely available tool, shifting economic value toward companies that use it best

Before looking at the company-specific implications of AI, we must develop a general framework that balances the transformative power of AI with its inherently uncertain rate of improvement, adoption and regulation. This framework rests on the assumption that AI represents one of the most powerful tools humankind has yet developed. However, because multiple companies (and countries) are developing the technology at the same time, with a new leader emerging every few months, it seems unlikely (but not impossible) that network effects or first-mover advantages will create monopolistic winners, such as happened with telephone networks (AT&T), information utilities (Google) or social networks (Facebook). Rather, it seems probable that intelligence itself will become a widely available utility with far more of the economic benefits accruing to the users of the technology than its creators. In this way, the eras of the printing press, railroads and broadband may be more useful referents.

Like other powerful tools, such as electricity, AI tremendously increases both productivity and efficiency, leading to an economy-wide shift that will favor early adopters. As companies deploy this technology, white-collar knowledge workers will face a similar fate to blue-collar workers during the era of factory automation and globalization, creating a backdrop of rising unemployment. While we expect employment to ultimately adjust, as it has after all technological shifts (for example, in 1800, more than 80% of the US workforce were farm workers versus less than 2% today2), the fast pace of AI’s rollout makes an unemployment shock far more likely.

Finally, as with the dawn of the atomic age, we must be aware of the risks created by the misuse of this powerful new tool by bad actors, including individuals, terrorist organizations, rogue states and, in this unique case, even AI itself.3

Stock Selection

Understanding how AI affects business models is now central to investment analysis

Within this economic framework, AI will impact most businesses in very different ways. In assessing both the risks and the opportunities presented by AI, our research places each company into one of five categories:

1) The Emerging Winners

Durable advantages will matter more than early hype

In the early days of a technological transformation, pundits and promoters spend a great deal of time trying to identify the emerging winners, often with disastrous results. For example, although the automobile transformed America, only three out of more than 3,000 automobile manufacturers survived.4 More recently, in March of 2000 there were 371 publicly traded internet companies.5 Five years later, the value of these companies had declined almost 90%, with more than half disappearing entirely. Even the largest and best-regarded companies of this era—Yahoo!, AOL and Cisco—have lost nearly all their relative value compared to the broader market, with two of the three companies effectively ceasing to exist.

When searching for emerging new winners, time and staying power are an investor’s best friend. For example, patient investors who resisted the hype of the early stages of the internet were rewarded with the opportunity to buy the handful of high-quality survivors, such as Amazon and Booking.com, at prices 80–90% below their March 2000 peaks. They also had the opportunity to invest in Google and Facebook when they went public at bargain prices many years later. In other words, even if you manage to identify a durable business that will emerge as a winner, buying it at a time of maximum hype is enormously risky.

At this early stage in AI’s evolution, we would avoid companies with little or no earnings, unproven business models and insatiable capital needs, such as foundational model providers. While we don’t dismiss the possibility that such companies may ultimately create durable competitive advantages, the inherent uncertainty around pricing power and switching costs creates huge risk. We are further cautious about the aggressive growth expectations that can turn even wonderful companies into mediocre investments. In the AI chip design space, for example, sky-high valuations assume that no viable competitors will emerge even though many of their largest customers (such as Google and Amazon) are already designing and using their own proprietary chips. Such high valuations leave no margin of safety or room for uncertainty.

Instead, we favor those few companies that have the raw materials and resources necessary to capitalize on the emergence of AI without taking existential risk. These materials and resources include proprietary data, large existing streams of cashflow, successful business models that will be enhanced through the application of AI, proven leaders and reasonable valuations.

2) The Enablers

Suppliers of AI infrastructure may benefit regardless of which technologies ultimately prevail

The next category includes those companies that will benefit from enormous levels of AI spending, currently estimated to rise from $427 billion last year to $758 billion in 2028,6 regardless of the returns on that spending. Companies in this category provide materials and equipment in a manner that is analogous to those (like Mr. Levi Strauss) who sold picks, shovels and clothing to the prospectors during the California gold rush. Our favorites in this category include chip manufacturers (known as foundries), the capital equipment companies that supply these foundries and, finally, designers and manufacturers of the analogue chips that are needed to translate information from the real world into the digital world. The Enablers also include non-technological or indirect beneficiaries such as the companies that provide the raw materials (including energy and copper) used to build out the required electrical power infrastructure for AI. Here, we focus on natural gas companies with low-cost and well-located reserves as well as mining companies with very long-lived, low-cost copper reserves.

3) The Users

Companies that successfully deploy AI could dramatically reduce costs and expand margins

Certain data intensive industries such as financial services and health insurance that currently rely on expensive knowledge workers (once referred to by Elon Musk as “the laptop class”7) have an enormous opportunity to retool their business models in ways that will dramatically reduce costs and improve profitability. However, because this retooling requires large investments to modernize their technology backbone, as well as tech-savvy managers and massive scale, most companies are likely to move too slowly, a textbook example of Clay Christensen’s Innovator’s Dilemma. The companies willing to cross this chasm and make the necessary investments will be competitively advantaged, leading to market share gains which could create a feedback loop that further disadvantages those left behind. In this category, company execution and scale matter more than industry selection.

4) The Insulated

Select businesses that remain largely insulated from technological disruption

This shrinking but important category was best described by Jeff Bezos when he said, “I very frequently get the question: ‘What’s going to change in the next 10 years?…I almost never get the question: ‘What’s not going to change in the next 10 years?’ And I submit to you that that second question is actually the more important of the two…” However, although such protected businesses face less disruption risk, they often grow slower or in a cyclical fashion. As a result, valuation discipline is critical. Fortunately, with all the hype around technology, many durable and insulated companies have been ignored and today sell at attractive valuations. Certain food suppliers, generic drug manufacturers, destination resort companies, and manufacturers of medical supplies trade at reasonable multiples with durable business models that seem protected from the threat of AI.

5) The Walking Dead

Technological shifts often destroy once-dominant business models

Because many once durable business models will certainly be undermined by the advent of AI, investment returns in the next decade will be built as much by avoiding the losers as by picking the winners. In many cases, research can identify a company’s strategic disadvantages long before they manifest in the financial statements, giving active investors time to get out. The demise of Kodak, once a component of the Dow Jones Industrial Average, is a good example. One had only to use a digital camera to quickly realize its tremendous advantages over film, most notably instant access to the image at a fraction of the cost. As can be seen in the table below, more than fifty million people had firsthand experience of digital photography by 2002 when annual sales of digital cameras surpassed film cameras. Yet even then, Kodak still ranked in the top third of the S&P 500 Index. However, by 2006, the shares had lost 90% of their value and the company filed for bankruptcy protection in 2012.

The same story could be told of the once iconic local newspaper companies whose profits were largely driven by classified advertising. The advent of specialized websites tailored to job, car and home buyers in the late 1990s doomed the classified business from the outset as these models were both cheaper and far more useful. Once again, active investors had time to get out while passive investors went down with the ship.

Finally, in some cases, the competitive threat can be more unexpected. For example, when the iPhone was launched, flashlight makers were not worried! In all such cases, research and active management are huge advantages as they allow investors to react when the handwriting is on the wall. Because the disruptive impact of AI will likely dwarf that of the internet, the advantage of being able to get out sooner may be even greater. Being confined by index weightings or, worse, trapped in illiquid investments can be an expensive disadvantage. To quote Kenny Rogers, “you got to know when to walk away and know when to run.”

| Year | Film Cameras Shipped (000s) | Digital Cameras Shipped (000s) | Kodak Mkt Cap (Approx. $B) |

| 1999 | 33,879 | 5,088 | ~20.5 |

| 2000 | 31,719 | 10,342 | ~11.8 |

| 2001 | 27,599 | 14,753 | ~8.5 |

| 2002 | 23,660 | 24,551 | ~10.2 |

| 2003 | 16,296 | 43,408 | ~7.2 |

| 2004 | 10,056 | 59,766 | ~9.1 |

| 2005 | 5,380 | 64,766 | ~6.6 |

| 2006 | 1,637 | 78,981 | ~2.6 |

Source: CIPA (Camera & Imaging Products Association) global shipment statistics, Eastman Kodak Form 10-Ks (shares outstanding) and NYSE historical year-end closing prices.

Conclusion

Periods of disruption reward flexibility, rigorous research, strict valuation discipline and active decision-making

The advent of AI represents a unique moment in human history that will profoundly transform the political, social, economic and investment landscape. While the rate of this transformation is uncertain, the transformation is unequivocally underway. During this time of significant change, a portfolio strategy that limits flexibility may, in the colorful language of Charles T. Munger, end up “like a one-legged man in an ass-kicking competition.” Investors should be wary of strategies that are passive, overly diversified, backwards looking, illiquid or lacking price discipline.

Instead, investors should shift away from richly valued indexes and illiquid strategies towards active, adaptable and flexible portfolio managers who can incorporate both the threats and opportunities posed by this powerful new technology into their research discipline and stock selection.

Christopher Davis, Chairman and Portfolio Manager

The Davis Research Methodology

Davis Advisors unique approach to building long-term wealth through investing in equities, including: what we look for in a company, how we arrive at an appropriate purchase price and the factors that may prompt us to sell a position.

PM Chris Davis on Investing in the Age of AI

As investors navigate one of the most consequential technological shifts in history, a practical framework for categorizing companies as " Winners", "Enablers" or "The Walking Dead"

For the sake of brevity, we will use the term artificial intelligence (AI) to represent the combined capabilities of what might be called the Intelligence Era. These include large language models, machine learning, agentic AI, and the prospect of so-called artificial general intelligence (AGI).

Data for these historical and modern workforce figures are sourced primarily from the U.S. Census Bureau and the U.S. Department of Agriculture (USDA).

See Agentic Misalignment: How LLMs could be insider threats https://www.anthropic.com/research/agentic-misalignment.

Sources from Wikipedia. https://en.wikipedia.org/wiki/Automotive_industry_in_the_United_States#:~:text=About%203%2C000%20automobile%20companies%

20have,%2C%20Henry%20Joy%2C%20William%20C

Source: “Burning Up; Warning: Internet companies are running out of cash—fast.” (Barron’s, March 20, 2000).

Source: Int’l Data Corporation (IDC) Worldwide Quarterly Artificial Intelligence Infrastructure Tracker.

CNBC interview with Elon Musk May 16, 2023.

Before investing in the Davis Funds or Davis ETFs, you should carefully consider the investment objectives, risks, charges, and expenses of the Funds. The prospectus and summary prospectus contains this and other information about the Funds. You can obtain performance information and a current prospectus and summary prospectus by visiting davisfunds.com, davisetfs.com, or calling 800-279-0279. Please read the prospectus or summary prospectus carefully before investing or sending money. Investing involves risks including possible loss of principal.

Shares of DUSA are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. There can be no guarantee that an active trading market for ETF shares will develop or be maintained, or that their listing will continue or remain unchanged. Buying or selling ETF shares on an exchange may require the payment of brokerage commissions and frequent trading may incur brokerage costs that detract significantly from investment returns.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact.

Davis Advisors is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy and approach. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this material. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate.

Objective and Risks. The investment objective of Davis New York Venture Fund is long-term growth of capital. The investment objective of Davis Select U.S. Equity ETF is long-term capital growth and capital preservation. There can be no assurance that a Fund will achieve its objective. Some important risks of an investment in the Funds are: stock market risk, common stock risk, market trading risk (DUSA), exchange-traded fund risk (DUSA), focused portfolio risk (DUSA), financial services risk; foreign country risk; China risk (DNYVF), headline risk; large-capitalization companies risk; manager risk; authorized participant concentration risk (DUSA), cybersecurity risk (DUSA), depositary receipts risk, emerging market risk (DNYVF), fees and expenses risk, foreign currency risk, mid- and small-capitalization companies risk, and shareholder concentration risk. See the prospectuses for complete descriptions of the principal risks.

The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. As of 3/31/26, the top ten holdings of Davis New York Venture Fund were: Capital One Financial, 6.03%; Coterra Energy, 5.57%; U.S. Bancorp, 4.87%; MGM Resorts, 4.00%; Alphabet, 4.00%; Viatris, 3.95%; CVS Health, 3.95%; Meta Platforms, 3.92%; Berkshire Hathaway, 3.88%; and Samsung Electronics, 3.71%.

As of 3/31/26, the top ten holdings of Davis Select U.S. Equity ETF were: Coterra Energy, 7.42%; Tyson Foods, 7.30%; Capital One Financial, 7.06%; U.S. Bancorp, 6.06%; Meta Platforms, 5.62%; Viatris, 4.96%; Alphabet, 4.81%; CVS Health, 4.28%; Amazon.com, 4.23%; and Texas Instruments, 4.22%.

Davis Funds and Davis Fundamental ETF Trust have adopted Portfolio Holdings Disclosure policies that govern the release of non-public portfolio holding information. These policies are described in the relevant Statement of Additional Information. Holding percentages are subject to change. Visit davisfunds.com, davisetfs.com, or call 800-279-0279 for the most current public portfolio holdings information.

The S&P 500 Index is an unmanaged index that covers 500 leading companies and captures approximately 80% coverage of available market capitalization. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue chip stocks. The Dow Jones is calculated by adding the closing prices of the component stocks and using a divisor that is adjusted for splits and stock dividends equal to 10% or more of the market value of an issue as well as substitutions and mergers. The average is quoted in points, not in dollars. Investments cannot be made directly in an index.

Distributor of Davis Funds is Davis Distributors, LLC

800-279-0279, davisfunds.com

Distributor of Davis ETFs is Foreside Fund Services, LLC

800-279-0279, davisetfs.com

Foreside and Davis Selected Advisers, LP, the Fund’s

investment adviser, are not related.

Investing in the AI Age

Winners, Enablers and the Walking Dead