Manager

Manager Video Commentary

Share

Key Takeaways

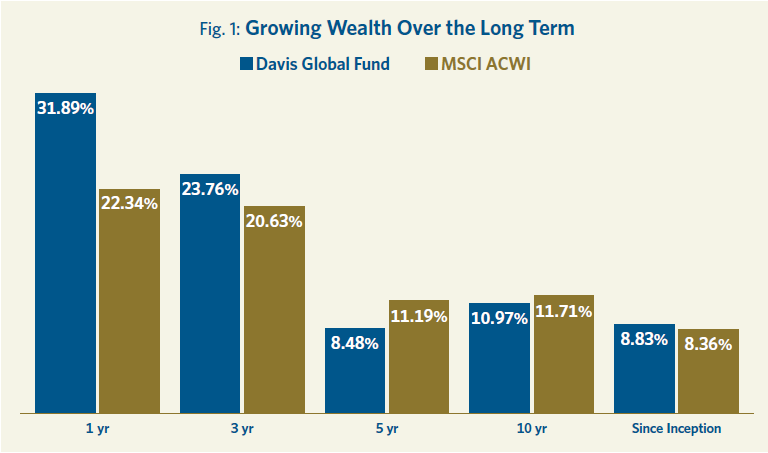

- Davis Global Fund (DGF) returned +31.89% in 2025, substantially outperforming the MSCI ACWI (All Country World Index) benchmark, as it has done on an annualized basis since inception.

- Our performance in 2025 was driven by strength in specific technology, financial and healthcare holdings. During the period we trimmed certain positions mainly on valuation and redeployed capital elsewhere.

- While our U.S. holdings represent 45% of the fund by market cap, we are underweight the benchmark in the U.S., where we believe valuations are elevated. However, we are significantly overweight the benchmark in China, where we see many interesting opportunities at attractive valuations.

- Our portfolio holds a small number of names with higher earnings growth rates and lower valuations on average than the index. This selectivity—our active share is 91%—is what makes us optimistic about the fund’s prospects.

The average annual total returns for Davis Global Fund’s Class A shares for periods ending December 31, 2025, including a maximum 4.75% sales charge, are: 1 year, 25.63%; 5 years, 7.43%; and 10 years, 10.44%. The performance presented represents past performance and is not a guarantee of future results. Total return assumes reinvestment of dividends and capital gain distributions. Investment return and principal value will vary so that, when redeemed, an investor’s shares may be worth more or less than their original cost. For most recent month-end performance, Click here or call 800-279-0279. Current performance may be lower or higher than the performance quoted. The total annual operating expense ratio for Class A shares as of the most recent prospectus was 0.95%. The total annual operating expense ratio may vary in future years. Returns and expenses for other classes of shares will vary.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. All fund performance discussed within this material refers to Class A shares without a sales charge and are as of December 31, 2025, unless otherwise noted. This is not a recommendation to buy, sell or hold any specific security. Past performance is not a guarantee of future results. The Attractive Growth and Undervalued reference in this material relates to underlying characteristics of the portfolio holdings. There is no guarantee that the Fund performance will be positive as equity markets are volatile and an investor may lose money.

Performance:

Power of Active Share

Davis Global Fund (DGF) posted a strong return of +31.89% in 2025, outperforming the +22.34% return of the MSCI ACWI benchmark by almost 1,000 points. The fund has outperformed the index on an annualized basis since its inception in 2004.

In this report we discuss the factors behind our performance as well as the contributors and detractors to those results. We go through some of the capital allocation decisions we have made and explain where we are seeing opportunities in the world.

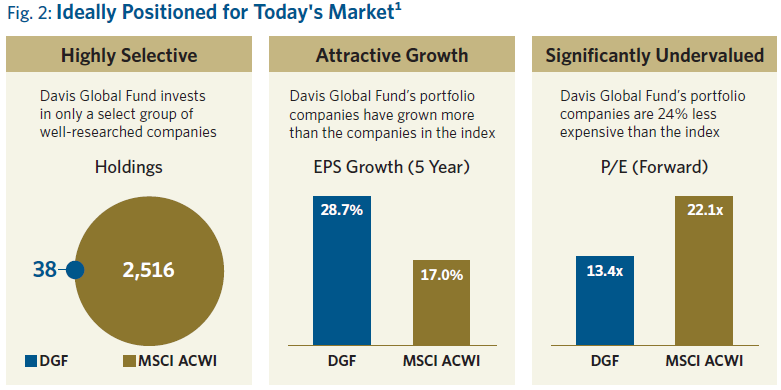

In general, we are very optimistic about the outlook for the portfolio. The three pillars of our optimism are outlined below—namely, our selectivity, and the high earnings growth potential of our portfolio companies together with their relatively low valuations compared to the index.

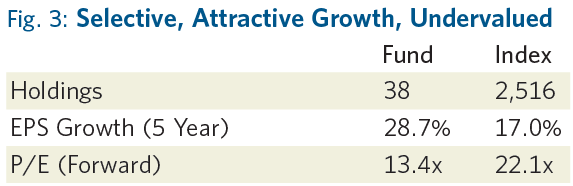

The fund’s portfolio holds only 38 names compared with more than 2,500 for the index. This means we are extremely selective. As a result, our portfolio has a much higher five-year average earnings per share growth rate than the index and yet is trading at a meaningful discount to the index on a forward price/earnings basis. We think this combination of higher growth and lower valuation bodes very well for future absolute and relative performance.

Among the factors driving our results in 2025 was strong performance by several of our technology holdings, including Samsung, AppLovin, Prosus (which owns Tencent), NetEase, Applied Materials and Alphabet (formerly Google). We also saw strength among the select financials that we own, including Danske Bank, Capital One and Ping An Insurance. Our healthcare names performed well too, especially CVS Group, which had a very strong year overall.

Among detractors from performance was Meituan, the Chinese food delivery company, where increased competition hurt results. Pinterest was also a detractor in the short period that we owned it after initiating a position late in the year.

Regarding capital allocation decisions, we made several valuation trims where we felt the margin of safety had narrowed due to strong performance. In technology, we trimmed our positions in Meta, Amazon and Samsung, all names that have continued to be very strong. We allocated capital to new buys, including AppLovin, which is one of the leaders in delivering ads for mobile gaming, a growing sector. We also started a position in Pinterest, as mentioned.

In financials, also due to valuation, we trimmed Capital One, Danske Bank and Berkshire Hathaway.

In healthcare we saw a great opportunity to add UnitedHealth, which is a name we owned in the past but had sold on valuation. During 2025 the stock fell 40% in just a single month, so we started a new position in it. We also sold out of our holdings in Quest Diagnostics and Humana.

In industrials and materials, we added Aumovio, a German car parts manufacturer, and JBS, a Brazilian meat processor. Aumovio, though not well-known, is an interesting company that was recently spun off from its parent, Continental. Spinoffs can be a promising area for low valuation buys. We also added to our positions in Full Truck Alliance, a digital platform that connects shippers and truckers in China, and U.S. food manufacturer Tyson Foods.

Finally, we initiated some new positions in the energy commodity space, including Coterra which owns oil and natural gas interests in the Permian Basin in Texas and natural gas interests in the Marcellus Shale in Pennsylvania. We trimmed our holding in Teck Resources, a global leader in copper production, due to its very strong performance in 2025.

We explained previously how different our portfolio is from the benchmark in terms of its selectivity, earnings growth profile and valuation. As a result of our active selection process, it also differs from the index in other key respects.

Country weightings are an example. Our single largest country weighting is the U.S. but we are underweight the U.S. relative to the index and relative to the U.S.’ share of global stock market capitalization. The U.S. today represents almost two-thirds of the global index because of its elevated equity market valuations. As a result, we have pivoted slightly away and repurposed some of our U.S. exposures into non-U.S. names, including in China where we are significantly overweight. Valuations are much lower there and we are seeing some very good opportunities in China.

Our sector weightings are also quite different from the index. We are overweight in consumer discretionary, financials and energy and very underweight in technology, partly because of our deliberately limited exposure to the Mag 7 group of technology names, which are among the top 10 stocks in the S&P 500 Index by market capitalization.

As a result, our individual holdings look very different than the index, and our active share—which measures the degree of difference between a portfolio's holdings and those of its benchmark index—is very high at 91%.

Investment Landscape:

Global Opportunity Set

Looking at today’s investment landscape, we are seeing selective opportunities across the major regions that we invest in.

The U.S. economy remains the most dynamic in the world and as a result, produces many innovative global leaders, of which we own several. However, valuations in the U.S. market are elevated and the market is top-heavy and highly concentrated. As a result, in the U.S. we are looking beyond the most expensive stocks and finding very specific opportunities in healthcare, industrial, financial and select technology names. At the same time, we are aware of the economic risks in the U.S., including the level of national debt, the fiscal deficit and the continuing risk of inflation, and are monitoring these factors closely.

In Europe we see many excellent multinational companies but also a region with structural headwinds, whether regulatory, demographic or cultural (for example, an aversion to risk-taking). Those obstacles have historically led to less innovation and lower growth than in the U.S. In fact, one of the major risks we are monitoring in Europe is the extent to which these trends will persist and continue to suppress growth and innovation.

Turning to Asia, as mentioned we are significantly overweight China. Outside the U.S., this is one of the most dynamic economies in the world with many competitive and tech-forward companies that we consider attractive and well-run. We are impressed by the major advancements that are coming out of China. In renewable energy, for example, some 80% of the world’s solar panels and 70% of its wind turbines are made in China. The country today has the world's largest electric vehicle market and is home to the world’s biggest EV manufacturer. Its economy has tremendous innovation and dynamism, yet Chinese companies are trading at very attractive valuations, hence our overweight in the country. There are risks, with the chief concern probably being geopolitical, and this is something we are watching closely.

Among our investments in China are consumer facing internet companies that we consider innovative leaders. We have a position in Tencent, the largest video game company in the world now and a leader in messaging and social media within China. We own this through holding company Prosus, which is listed in Europe. We are invested in NetEase, the second largest video game company in China. We also own Meituan, the food delivery company, and DiDi, the ride-sharing leader in China with about 70% of the market.

Another major area of focus in China is life insurance. This is an interesting space. It is under the radar now, but we believe it is due for powerful long-term secular growth over the next decade or more as Chinese households pivot away from investing savings in property and direct them towards insurance products. We have a position in Ping An Insurance, the second largest insurance company in China. We also hold AIA, a Pan-Asian life insurer that has been in business for over a century.

Any discussion of investment opportunities needs to address AI. We look at this theme or segment through a value investors lens, which means we look for opportunities where the risk-reward is very positive. For example, one way that we approach investing in AI is to identify where the bottlenecks are. These areas include power generation, chip-making equipment and memory chips themselves. In terms of power, we have looked at natural gas as the main source of energy to power data centers and, as a result, own Tourmaline, a major Canadian natural gas company, and Coterra, which owns natural gas interests in the Marcellus Shale. We own Applied Materials, a leader in chip-making equipment. We also own Samsung, a major manufacturer of memory chips. It was trading at a very low valuation last year, and we managed to build a large position. This year, as the market has recognized the importance of high bandwidth memory, Samsung’s stock has done very well.

On the same theme we also look for companies with huge user bases that can apply AI and reap its rewards—for example, Meta, Amazon and Alphabet. Meta, to name one, has 3.5 billion daily users, which means half the world's population is using a Meta product daily. Meta is a major potential beneficiary of the use of AI, as are Alphabet and Amazon.

Finally, healthcare is also an area of great interest to us, and one where we have been spending a lot of time. In this group we own Viatris, a large manufacturer of generic pharmaceuticals, and CVS Group, a diversified healthcare major, both U.S.-based.

Putting it all together, we believe the fund’s structural characteristics are compelling—specifically, the selectivity of our investment process coupled with the fact that our portfolio companies have a materially higher earnings growth rate than the index average while trading at a meaningful discount to it.

This underpins why we are so optimistic about our prospects going forward.

Together on This Journey

For more than 50 years, Davis Advisors has navigated a constantly changing investment landscape guided by one North Star: to grow the value of the funds entrusted to us. We are pleased to have achieved strong results thus far and look forward to the decades ahead. With more than $2 billion of our own money invested in our portfolios, we stand shoulder to shoulder with our clients on this long journey.2 We are grateful for your trust and are well-positioned for the future.

Five-year EPS Growth Rate (5-year EPS) is the average annualized earnings per share growth for a company over the past 5 years. The values shown are the weighted average of the 5-year EPS of the stocks in the Fund or Index. Approximately 17.99% of the assets of the Fund are not accounted for in the calculation of 5-year EPS as relevant information on certain companies is not available to the Fund’s data provider. Forward Price/Earnings (Forward P/E) Ratio is a stock’s price at the date indicated divided by the company’s forecasted earnings for the following 12 months based on estimates provided by the Fund’s data provider. These values for both the Fund and the Index are the weighted average of the stocks in the portfolio or Index.

As of 12/31/25, Davis Advisors, the Davis family and Foundation, our employees, and Fund directors have more than $2 billion invested alongside clients in similarly managed accounts and strategies.

This material is authorized for use by existing shareholders. A current Davis Global Fund prospectus must accompany or precede this material if it is distributed to prospective shareholders. You should carefully consider the Fund’s investment objective, risks, charges, and expenses before investing. Read the prospectus carefully before you invest or send money

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact.

Davis Advisors is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy and approach. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate.

Objective and Risks. The investment objective of Davis Global Fund is long-term growth of capital. There can be no assurance that the Fund will achieve its objective. Some important risks of an investment in the Fund are: stock market risk: stock markets have periods of rising prices and periods of falling prices, including sharp declines; common stock risk: an adverse event may have a negative impact on a company and could result in a decline in the price of its common stock; foreign country risk: foreign companies may be subject to greater risk as foreign economies may not be as strong or diversified; China risk – generally: investment in Chinese securities may subject the Fund to risks that are specific to China including, but not limited to, general development, level of government involvement, wealth distribution, and structure; headline risk: the Fund may invest in a company when the company becomes the center of controversy. The company’s stock may never recover or may become worthless; depositary receipts risk: depositary receipts involve higher expenses and may trade at a discount (or premium) to the underlying security and may be less liquid than the underlying securities listed on an exchange; foreign currency risk: the change in value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency; exposure to industry or sector risk: significant exposure to a particular industry or sector may cause the Fund to be more impacted by risks relating to and developments affecting the industry or sector; emerging market risk: securities of issuers in emerging and developing markets may present risks not found in more mature markets. As of 12/31/25, the Fund had approximately 32.6% of net assets invested in securities from emerging markets; large-capitalization companies risk: companies with $10 billion or more in market capitalization generally experience slower rates of growth in earnings per share than do mid- and small-capitalization companies; manager risk: poor security selection may cause the Fund to underperform relevant benchmarks; fees and expenses risk: the Fund may not earn enough through income and capital appreciation to offset the operating expenses of the Fund; and mid-and small-capitalization companies risk: companies with less than $10 billion in market capitalization typically have more limited product lines, markets and financial resources than larger companies, and may trade less frequently and in more limited volume. See the prospectus for a complete description of the principal risks.

The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. As of 12/31/25, the top ten holdings of Davis Global Fund were: Samsung Electronics, 6.11%; Ping An Insurance Group, 5.79%; Trip.com Group, 5.12%; Prosus, 5.12%; Full Truck Alliance, 4.44%; Viatris, 4.31%; DiDi Global, 4.25%; Capital One Financial, 4.08%; Markel Group, 3.96%;

and Meta Platforms, 3.77%.

Davis Funds has adopted a Portfolio Holdings Disclosure policy that governs the release of non-public portfolio holding information. This policy is described in the Statement of Additional Information. Holding percentages are subject to change. Visit davisfunds.com or call 800-279-0279 for the most current public portfolio holdings information.

The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (MSCI) and S&P Global (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaim all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of such damages.

The “Magnificent 7” is a group of seven dominant, high-performing U.S. technology companies that have a significant influence on the stock market. The companies that make up the Magnificent 7 are: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

We gather our index data from a combination of reputable sources, including, but not limited to, Lipper, Clearwater Wilshire Atlas, and index websites.

The MSCI ACWI (All Country World Index) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets throughout the world. The index includes reinvestment of dividends, net foreign withholding taxes. Investments cannot be made directly in an index.

After 4/30/26, this material must be accompanied by a supplement containing performance data for the most recent quarter end.

Item #4719 12/25 Davis Distributors, LLC 2949 East Elvira Road, Suite 101, Tucson, AZ 85756 800-279-0279, davisfunds.com

Global Fund

Annual Review 2026

Managers