Manager

Share

Executive Summary

- For the 12 months ended December 31, 2023, Davis International Fund (DIF) returned 5.11% compared with 15.62% for the MSCI ACWI (All Country World Index) ex US—for an underperformance of 10.51%. In this report, we discuss the factors contributing to DIF performance. We also delve into three of the year’s more compelling refrains.

- Normalization of interest rates was a dominant theme of the economic landscape in 2023, as some investors began to re-realize that there’s no such thing as easy money. “The free-money” bubble that enthralled many investors for more than a decade has burst, finally. But as we return to reality, we still have a way to go toward unravelling the distortions this bubble wrought upon financial markets.

- While the weak real estate market in China is leading to slower growth, the high down payment requirements to buy a home means it probably will not lead to a banking crisis. Moreover, the growing government support for the economy coupled with the low valuations for our Chinese holdings is increasing the odds of future outperformance.

- 2023 may be remembered for the start of an early but widespread generative artificial intelligence (AI) frenzy. We believe the economic and societal impact of near-term generative AI advances will be significant and pervasive. While the potential exists for AI to reshape all aspects of our industrial economy, we are still in the early stages of the journey.

The average annual total returns for Davis International Fund’s Class A shares for periods ending March 31, 2024, including a maximum 4.75% sales charge, are: 1 year, 0.65%; 5 years, -0.92%; and 10 years, 1.27%. The performance presented represents past performance and is not a guarantee of future results. Total return assumes reinvestment of dividends and capital gain distributions. Investment return and principal value will vary so that, when redeemed, an investor’s shares may be worth more or less than their original cost. For most recent month-end performance, click here or call 800-279-0279. Current performance may be lower or higher than the performance quoted. The total annual operating expense ratio for Class A shares as of the most recent prospectus was 1.09%. (The Adviser is contractually committed to waive fees and/or reimburse the Fund’s expenses to the extent necessary to cap total annual fund operating expenses of Class A shares at 1.05%. The expense cap expires March 1, 2025.) The total annual operating expense ratio may vary in future years. Returns and expenses for other classes of shares will vary. The Fund’s performance benefited from an IPO purchase in 2014. After purchase, the IPO rapidly increased in value. Davis Advisors purchases shares intending to benefit from long-term growth of the underlying company; the rapid appreciation of the IPO was an unusual occurrence.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. All fund performance discussed within this material refers to Class A shares without a sales charge and are as of 12/31/23, unless otherwise noted. This is not a recommendation to buy, sell or hold any specific security. Past performance is not a guarantee of future results. The Attractive Growth and Undervalued reference in this material relates to underlying characteristics of the portfolio holdings. There is no guarantee that the Fund performance will be positive as equity markets are volatile and an investor may lose money.

Current Positioning, Long-Term Performance and Recent Results

For the 12 months ended December 31, 2023, Davis International Fund returned 5.11% compared with 15.62% for the MSCI ACWI (All Country World Index) ex US—for an underperformance of 10.51%. In this report, we discuss the contributors and detractors to DIF performance and delve into what we believe was the biggest shift in the investing environment during the past decade. We also address the geography that has been the biggest headwind of the past three years, as well as a major new technology (AI) that likely will be the biggest technological breakthrough of the past 50 years.

Contributors to 2023 Performance

The largest contributor to DIF performance in 2023—and the fund’s largest position—is Danske Bank. Denmark’s largest bank returned 42% for the year. While financials as a sector underperformed the benchmark in 2023, much of the latent potential in Danske Bank was realized during this year. Entering the year, Danske Bank was valued at only 6x owner earnings and 0.7x book value, which was too cheap given the strength of the franchise and Denmark's healthy economy. The uncertainty surrounding the investigation into compliance lapses at Danske’s Estonian subsidiary was lifted in December 2022 in an announced agreement with regulators. Since then, operating results in 2023 have been solid with good growth in net interest income. In addition, low credit losses led to good earnings growth. Even after the strong stock performance, Danske Bank today still trades at only 8x 2024 owner earnings and 0.9x book value, leaving room for even more multiple expansion going forward. Earnings growth likely will be helped by further cost cutting and market share gains now that the bank’s regulatory concerns have been addressed. While we should expect some credit normalization over time given very low current loan losses, we also know that Danske is overcapitalized with a Common Equity Tier 1 (CET1) ratio of 19%, which is well above the company’s regulatory requirement of 14.3% and management’s target of 16%. Becoming more capital efficient will further drive earnings growth. Finally, future dividend yields will be between 7% and 8% at the current share price. As a result, Danske Bank is a rare combination of safety and high return potential, and warrants a large position.

Semiconductor companies Tokyo Electron and Samsung were up 87% and 42%, respectively, as investors are starting to look past the post-COVID weakness to focus on the strong long-term outlook for semiconductors. Tokyo Electron is benefiting from all the investments made across the world to build semiconductor manufacturing capacity often with the aid of government subsidies. As the world’s largest manufacturer of memory chips, Samsung is among those heavily investing in semiconductor manufacturing capacity. The digitization of the global economy—including in the technology, media, industrial and consumer sectors—is driving demand for Samsung’s memory chips. In particular, the dramatic increase in the level of computing power that’s necessary to develop artificial intelligence (AI) products is driving demand for high bandwidth memory (HBM), where Samsung is one of the leaders with an estimated 46-49% market share.1 Finally, Chinese industrial automation company Hollysys Automation rose 60% after receiving a takeover proposal from a private-equity firm. Given that at mid-year 2023 Hollysys was trading at only 8x owner earnings with 55% of its market cap in cash on the balance sheet, it was not a big surprise that the company has received multiple takeover offers.

Detractors to 2023 Performance

Detractors to DIF performance include the Chinese internet companies JD.com and Meituan, which were down 48% and 53% respectively. Investors reacted to the combination of a slower-than-expected economic recovery post-COVID, and competition from Bytedance as it seeks to grow its e-commerce and restaurant marketing businesses in China. Through the first nine months of 2023, JD.com sales were up 4% but earnings jumped 35% because of controlling expenses that drove up margins. As a result, JD.com today trades at 7x 2024 owner earnings with the opportunity to see much stronger revenue growth as economic growth accelerates. Meituan, on the other hand, continued to see strong revenue growth with sales up 27% for the first nine months of the year. Operating margins, however, were impacted by an aggressive response to Bytedance’s incursion into Meituan’s in-store marketing business. Meituan spent on consumer subsidies and lowered the commission rate charged to restaurants to keep merchants on the Meituan platform. Meituan is trading at only 9x 2024 owner earnings and the stock price is now within 10% of its initial public offering price in 2018 despite revenues being greater than 4 times their level of five years ago. The market appears to have overreacted to the competitive threat from Bytedance.

While Danske Bank was up more than 40% in 2023, Ping An Insurance was down 28%, AIA Group was down 20%, Julius Baer was flat and DBS Group was up only 7%. As a result, financials as a group underperformed the benchmark. Despite the weaker Chinese macroeconomic backdrop, Ping An’s core business of life and health insurance performed well. The value of new business written in the first nine months of 2023 rose 41% year over year. Weaker bond yields and equity returns, however, impacted the asset management segment, leading to a 10% decline in profits. Ping An’s core life and health insurance business is performing well, growing steadily and taking share in a large market with a bright long-term outlook. Trading at 4x 2024 owner earnings with an 8% dividend yield, the life and health insurance leader in China looks very undervalued.

The Swiss wealth manager Julius Baer underperformed its banking peers based on concerns with a single private credit portion of its book. While losses are probable, the magnitude of those losses remains small relative to Julius Baer’s loan book and balance sheet. Trading at 9x 2024 owner earnings with a 5.5% dividend yield, this premier global wealth manager also looks attractive.

Current Perspective on Global Markets

Return to Rationality After a Decade of Distortion

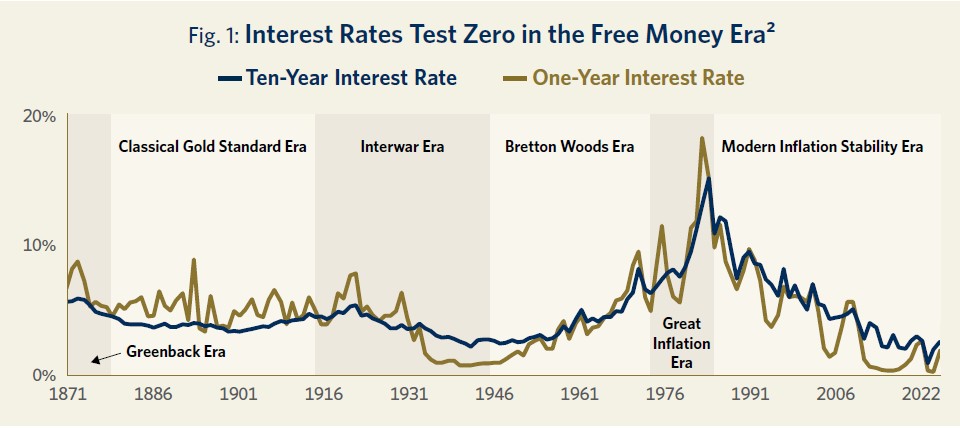

The key economic event of the past year has been the normalization of interest rates. The easy-money bubble began to burst on March 16, 2022, when the Federal Reserve announced the first of 11 consecutive increases in the federal funds benchmark rate, the steepest change ever. As Figure 1 shows, during this so-called free money era, both short- and long-term interest rates approached their lowest levels in recorded history.

As the cost of money approached zero despite huge increases in money supply, these policies created significant market distortions during which assets were mispriced, risks ignored, inflation allowed to metastasize and valuation discipline penalized. Given the sheer magnitude of these distortions, the great unraveling that began in 2022 still has a long way to go. While we do not expect further interest rate increases in the short term—and, in fact, believe that interest rates may come down in the short term as inflation stabilizes at more normal levels—the free money bubble that began in 2009 has burst and the reckoning will continue.

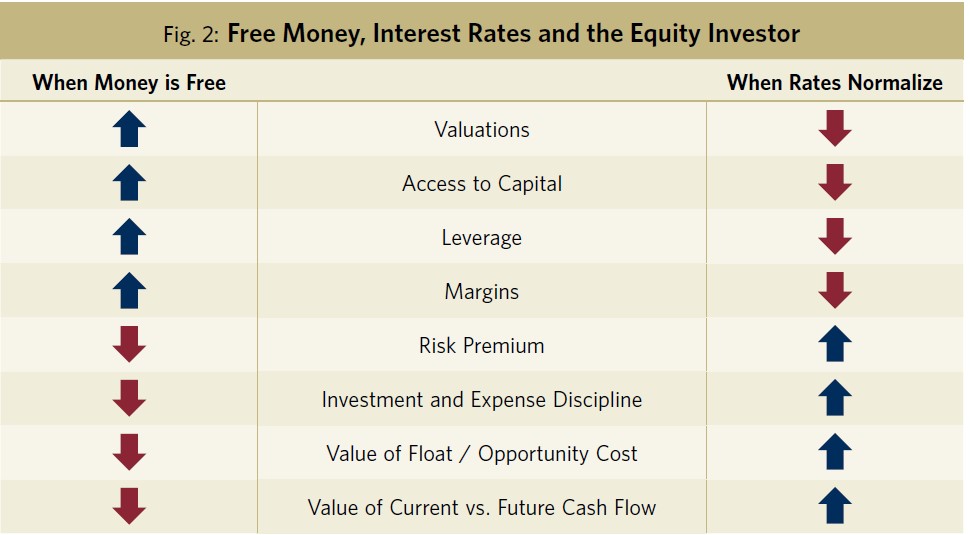

For investors like us, who have always adhered to a valuation discipline, this period of unraveling represents an overdue but volatile return to normalcy after more than a decade of delusion. As we return to the reality of financial markets, we are encouraged that the companies we own (including our carefully selected banks) are well-positioned for the current ever-changing environment. Although short-term results are unpredictable, it should come as no surprise that investors are once again seeking durability, profitability, cash production, valuation and balance sheet strength as these characteristics allow companies to navigate a period of higher interest rates and economic uncertainty better.

As Figure 2 illustrates, reverting to more normal interest rates creates a relative headwind for many of the darlings that led the market for so long; and it may create a tailwind for the type of durable, attractively valued businesses that lie at the heart of our investment discipline.

For investors who believed that the period between 2008 and 2022 represented a new normal in which money was free, valuation was irrelevant and profitless growth could go on forever, the reckoning is already wreaking havoc. Mismanaged banks like Silicon Valley and First Republic (neither of which we owned) that prioritized earnings growth over risk control collapsed; leveraged pension funds in the U.K. required government bailouts; and former market darlings like Spotify, Shopify, Square, Zoom, WeWork, Robinhood and Peloton are down approximately 50-100% from their all-time highs.

As the effects of higher-cost capital roll through the system, the examples above are just a prologue. We expect many well-known venture capital and private equity funds that have been slow to write down the carrying value of portfolio holdings probably will report dismal results in the years ahead. Companies with large amounts of maturing low-cost debt may have trouble refinancing at rates that don’t erode their profitability, assuming they can refinance at all. Holders of commercial real estate that were leveraged when capital rates were below today’s risk-free rate likely would have their equity significantly diminished or even wiped out. Above all, for the first time in our nation’s history, interest payments on our country’s growing debt surpassed defense spending and are poised to rise steeply as maturing low-cost debt is refinanced at higher rates. This growing interest rate burden in the face of a somewhat dysfunctional state of affairs in our nation’s capital reinforces our focus on durable and resilient business models.

Interestingly, while many of the examples above are well known, the largest and most important losses do not seem to be getting much attention. Perversely, these losses reside precisely in the portion of investors’ portfolios that have been considered the safest and least volatile. After more than 40 years of falling interest rates, investors came to view government bonds as pillars of safety that could be relied on to preserve value in times of volatility and uncertainty. We have strongly disagreed for years, calling bonds purchased at low interest rates “return-free risk” rather than “risk-free return.” From March 2022 until today, long-term government bonds have declined 25% to 35%. These losses in the face of relatively high inflation remind us why veteran investors whose careers extended into the half century of rising interest rates—which preceded four decades of falling rates—have called bonds “certificates of confiscation.”

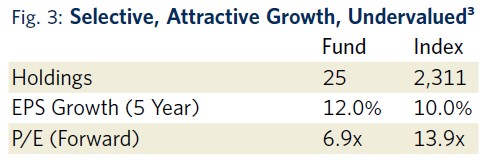

While recent returns have been strong, our portfolio remains significantly undervalued when compared to the market averages. The table in Figure 3 indicates that the carefully selected group of companies that comprise DIF portfolio trade at only 6.9x forward earnings—a 50% discount to the MSCI ACWI ex US, despite having grown their earnings per share faster than the index at 12.0% per year in the past five years. This rare combination of durable growth and discount prices is a value investor’s dream that positions us well for the years ahead.

China—Challenges and Opportunities

Pundits have been predicting the impending collapse of the Chinese economy for the past couple of decades. And while they have been wrong thus far, cautious investors should always re-examine the data and their prior expectations. Could the pundits be right this time? The data does not support such a pessimistic view, and we continue to see the Chinese economy as sound. Certainly, the current real estate downturn and long-term aging of the population are headwinds. Nor are we making short-term forecasts, or opining on whether the International Monetary Fund’s forecast of 4.2% gross domestic product growth in 2024 is too high or low. However, when looking at the data we do see an economy that has many proven strengths and though China like all economies has its challenges, these do seem manageable.

The main challenge to growth for the past couple of years has been the weak real estate market. Real estate directly accounts for 11% of China’s GDP4 and indirectly accounts for about 22%, down from 25% in recent years.5 In August 2020, the government imposed strict leverage limits on selected property developers. These policies, known as the “three red lines,” were established against a backdrop of growing debt levels, rising land prices and booming sales, which led to rising concern about housing affordability. The forced deleveraging of these highly indebted property developers resulted in a significant pullback in real estate investment and sales. As Figure 4 illustrates, contribution of property-related activities to GDP growth in real estate was a 4% drag on growth in 2022 (and the main reason GDP growth was only 3%). And while it was also a headwind to growth in 2023, this improved to 2% and the economy still managed about 5.2% growth in 2023. Expectations are for real estate to still be a headwind to GDP growth in 2024, as China’s problems in its residential property sector seem to be diminishing.

While the impact on the economy’s growth is manageable could the real estate downturn in China lead to a banking crisis as it has in other economies? That appears highly improbable for four main reasons: 1) the loan-to-value ratios for mortgages in major cities is approximately 40%, 2) mortgages are unlimited personal liabilities—risk of default is very low, 3) developer loans represent less than 6% of total loans and are secured and 4) the capital-adequacy ratio is more than 15% for the banking system.6 This means that housing prices would on average need to fall by more than half for homes to be worth less than the equity already owned in the home. It also means that homeowners don’t have any incentive to turn in the keys and default on the mortgage because it is a personal liability. Moreover, although developer loans generate a lot of media attention, they represent only 6% of total loans, and they are collateralized. Finally, with 15% capital ratios, banks are well capitalized. This is not to say that housing is not currently a headwind for the economy, just that it likely will not precipitate a banking crisis.

New home prices have been weak in 2023 and in December they were down 0.4% year over year after falling 0.2% year over year in November. As a result, authorities have cut the mortgage down payment requirement and loosened the residency requirements in major cities where they have been the strictest in the past—such as Beijing, Shanghai, Shenzhen and Guangzhou. Suzhou, the largest city in Jiangsu province, even removed all restrictions, allowing buyers to purchase as many homes as they can afford.7 When these supportive measures led by local governments will result in a troughing, and eventually a rebound in housing prices, depends on many factors but the likelihood of success has been rising as the national government in Beijing is increasingly supportive of the broader economy. Beijing decided to increase government spending in 2024 by an additional 1 trillion yuan ($140 billion) for key infrastructure projects such as flood control, healthcare and transportation projects.8 In January 2024, the central bank cut the bank reserve ratio requirement sooner—and by a larger percentage than expected—which enabled banks to make an additional 1 trillion yuan ($140 billion) in loans.9

Our Chinese holdings such as Meituan, JD.com, Ping An Insurance and Tencent (owned through Prosus and Naspers) are among our cheapest holdings. Currently, for example, JD.com trades at a forward price/earnings multiple of 7x, Meituan at 12x, Ping An at only 4x and Tencent at 9x. These are very attractive starting valuations for high-quality companies with strong franchises and outlooks. Risks such as the current macro environment, competition and geopolitical tensions do exist, but we believe the risk-reward ratio is very positive.

How Have We Positioned the Portfolio for AI?

Nvidia Corporation’s CEO, Jenssen Huang has remarked: “Generative AI is the single most significant platform transition in computing history. In the last 40 years, nothing has been this big. It’s bigger than the PC, it’s bigger than mobile, and it’s gonna be bigger than the internet, by far.”

This is just one of many grand prognostications we have heard during the past year following the launch and subsequent explosion in popularity of OpenAI’s ChatGPT service. Hearing similar sentiments around the advancements in generative artificial intelligence (AI) echoed broadly by industry operators we expect led us to spend significant time this year to better understand ChatGPT’s undergirding technology and its potential implications across industries.

Generative AI Extends Earlier Advancements in AI

Generative AI is the broad term used to classify AI technologies that are capable of creating original content. Generative AI burst into the mainstream investing discourse in 2022 driven by the release and rapid adoption of text-to-image generator services like MidJourney and large language model based chatbots such as ChatGPT. Upon its release in November 2022, ChatGPT became the fastest-growing consumer internet app with an estimated 100 million monthly users in just two months.

Excitement around AI advances is not new. During the past decade, the field of AI has made tremendous strides, catalyzed by a series of breakthroughs in “deep learning”—an AI technique that teaches computers to process data in a way that’s inspired by the human brain.10 These breakthroughs enabled the proliferation of “traditional” AI11 models that are designed to make narrow predictions based on patterns learned from large quantities of training data. Traditional AI advancements drove rapid improvements in state-of-the-art applications such as computer vision, natural language processing and recommender systems. Companies such as Alphabet and Meta have been at the forefront of building deep pools of AI talent and incorporating AI technology to supercharge the performance of products such as Google search and Facebook newsfeed.

In addition to impressive innovations in deep learning algorithms and model architectures, a core driver of AI progress over the last decade has been the durability of performance gains from rapidly scaling the size of deep learning models. Successfully building larger models requires greater amounts of relevant training data and more computing power, typically in the form of chips that can process data in a highly parallel fashion, such as graphics processing units (GPUs). Although aggregating more data and utilizing more GPUs becomes increasingly expensive, the performance improvements from model scaling continue to justify ever larger budgets for training models across the industry.

The importance of model scaling has certainly carried over to generative AI systems. OpenAI’s GPT-3 large language model released in 2020 was more than 100 times larger by parameter count, and it trained more data than GPT-2 released only a year earlier. In addition, GPT-3 is more than 1,500 times larger than GPT-1, which was released in 2018—one year after publication of the original algorithm innovation that enabled large language models.

We believe the economic and societal impact of generative AI advances will be significant and pervasive in the near term. Assuming that generative AI development continues to progress at anywhere near its current pace—a big assumption on our part as outside observers—it’s also easy to see how generative AI has the potential to reshape all aspects of our industrial economy profoundly. However, exactly how future generative AI breakthroughs will unfold is likely unknowable at this stage, even to leading practitioners. While the corresponding impact on individual businesses will be path dependent and thus very uncertain, generative AI will undoubtedly disrupt a number of business models and competitive moats even as it creates new business opportunities. This makes it critical for us to continue following AI developments closely both to mitigate risks in the portfolio and identify underappreciated opportunities.

Unsurprisingly, most of the market’s AI attention today seems focused on near-term winners and losers. Despite what promises to be widespread change across industries longer-term, there is simply significantly more near-term impact on the subset of hardware and software companies directly tied to actually building and running AI models—the AI technology stack. Nvidia, the leading supplier of advanced, built for AI GPUs, is the posterchild for this phenomenon and has seen its stock price increase approximately 239% in 2023 driven by the remarkable growth in its datacenter revenues. Our view is that many of the obvious direct AI beneficiaries have valuations that already bake in aggressive top- and bottom-line expectations. Our preference in the AI technology stack has been to focus on innovative, high-quality companies where we believe meaningful incremental AI-related revenue and earnings likely will manifest over the next few years, but where valuations don’t yet reflect the expected tailwinds from increased AI activity.

The semiconductor industry looks poised to benefit from the tremendous compute and specialized memory requirements of generative AI. Our investments in Samsung and Tokyo Electron strike us as compelling given their foundational importance to the production of advanced chips.

On top of the AI technology stack sits the application layer. We are generally more cautious about underwriting explicit AI driven theses in the application layer. Trying to identify which potential generative AI products find product market fit, the strength of the moats around those products and estimating the long-term economics those products will support seems highly speculative at this stage. At a high level, technologically sophisticated incumbents look well positioned to leverage generative AI as an innovation to sustain their competitive positions. Generative AI products are expensive to build and run; they benefit from large amounts of proprietary data, and will still require efficient, large-scale distribution. Some of the initial applications investors appear most excited about are near-term product enhancements to already popular software platforms, as exemplified by Microsoft’s 365 Copilot which embeds ChatGPT-like features throughout Microsoft’s Office suite. Industry observers are already suggesting that the incremental revenues associated with this AI add-on will exceed $10 billion within a few years. While we recognize the potential for products like 365 Copilot, we think expectations for the product are already sizable.

Our approach in the AI application layer to date has been to focus on companies with the ingredients to successfully develop and distribute generative AI products, but whose exact plans remain vague and investor expectations do not yet incorporate the impact of new products. Tencent with its strong positions in messaging, social media, cloud computing and video games has the potential to be a major beneficiary of generative AI. U.S. companies were early in researching generative AI and incorporating it into their services. A good example is Meta, owner of Facebook, Instagram and WhatsApp. Meta is in the midst of using generative AI to: 1) reduce the costs drastically for advertisers to create and run highly optimized and successful advertising campaigns and 2) enable merchants on Meta’s platforms to engage users via AI chat more efficiently. Tencent has a similar opportunity in China where generative AI should result in advertisers and merchants spending more to advertise on WeChat, which could lead to more commerce taking place on the messaging app. Moreover, Tencent has two other major areas of opportunity to monetize generative AI. Most of the training and inferencing of large-scale AI models today occurs on hyperscale cloud services and this is a substantial opportunity for Tencent Cloud. Video game development is also a beneficiary where generative AI can both lower programming costs and greatly enhance gameplay by making interactions with in-game characters much more natural.

We're Still Early

The earliest generative AI products have been out in the market for just over a year. Leading-edge U.S. incumbents like Microsoft and Alphabet along with Chinese leaders including Baidu, Tencent and Alibaba are just now rolling out their initial generative AI products, and many slower-moving large enterprises are still in the prototyping phase. We are at the earliest stages of the generative AI journey, and despite what stock market prices may be suggesting today, how this journey unfolds is largely up in the air. Both the rate at which generative AI capabilities improve and the degree to which costs to deploy them come down are big unknowns. Moreover, consumer interest in generative AI has yet to be fully validated. Everyone’s assumptions, including ours, are subject to change. We will continue to pay close attention to developments in AI, engage with companies at the forefront of AI innovation and remain flexible in our thinking as we look for attractive investment opportunities related to AI.

Notes on Holdings

KE Holdings Inc.

KE Holdings (aka Beike) is China’s largest omni-channel residential real estate brokerage platform, with greater-than 30% market share in existing home transactions. The company owns and operates Lianjia, the country’s largest real estate broker with 5,500 stores. The company has franchise-like relationships with a network of 40,000 independent non-Lianjia third-party stores and runs the most popular online real estate listings platform in China. With nearly 400 thousand real estate agents operating within its ecosystem, the company has established itself as a clear market share leader in the largest cities in China, while building a strong brand around service, quality and trustworthiness. Beike’s extensive reach and efficient agent operations means it maintains the most comprehensive, accurate and up to date local real estate listings and property data in the market. This is a significant competitive advantage in a country where multiple listing service (MLS)-like offerings do not exist. Initially specializing in agency services for existing home transactions, the company has leveraged its store footprint and agent network to offer brokerage services for new home transactions—that is, helping real estate developers sell their properties—as well as home renovation and furnishing services.

We believe the current malaise in China’s property sector has provided an attractive opportunity to initiate a position in Beike. While Beike’s near-term prospects will undoubtedly be impacted by a weak housing market, we find the company well-positioned for long-term growth given its high exposure to existing home transactions and home renovation and furnishing services, two areas within residential property that will benefit from structural tailwinds going forward. Even its new homes business appears reasonably insulated from the structural decline of new home construction given its scant exposure to lower-tier cities where most of the oversupply issues are concentrated. While the continued pressure on housing prices represents a risk to overall commission revenues, we believe that some degree of further declines are already factored into the stock price, which trades at 12x forward owners’ equity. With strong financial resources including $9 billion of net cash on its balance sheet—worth more than half of its current market capitalization of $17 billion—and solid profitability in a depressed housing market, we believe Beike will gain meaningful share from distressed competitors in the event of a prolonged housing recession.

Fila

Fila Holdings Corp. designs and markets the Fila sportswear and footwear brand globally. While the origin of the brand is Italian, Fila Korea’s management led a buyout of the global operations and now the Yoon family owns 35% of the group while holding the top management positions. Fila primarily targets a younger clientele in the mid-priced casual-wear segment. They also have a strong franchise in tennis and own a controlling stake in publicly traded Acushnet, makers of Titleist and FootJoy golf products.

Fila is in the middle of a five-year multi-pronged strategy to revitalize its brand. They’re increasing the mix of direct-to-customer channels (e-commerce and own stores) in the U.S. and Korea. This should be margin accretive and improve inventory management. The company also is re-branding and aiming for a unified global marketing strategy to elevate brand awareness and introduce the brand to a younger audience. The five-year plan also realigns Fila’s commitment to shareholders by increasing the dividend payout from 5% in 2019 to 50% by 2026.

Once the brand realignment and inventory destocking issues are resolved, Fila should be able to grow revenues by mid-single digits and get some operating leverage from increasing margins. The stock trades at less than 10x current year’s earnings. If we subtract the publicly traded value of Acushnet, then Fila equity is currently valued at less than zero. We think the substantial holding company discount will narrow as Fila group increases shareholder return based on consolidated earnings. The key risks here would be Fila’s inability to deliver on the brand revamp and a severe slowdown in the China market, as that remains a lucrative business for Fila.

Near-Term Outlook

In an uncertain world where there are worries about a shifting geopolitical landscape, rising interest rates (both inflation and deflation), environmental concerns and high sovereign debt levels we believe investing in companies remains the best long-term strategy for creating and preserving wealth. We focus on companies with proven cash generation power run by experienced and driven management teams that can adapt to their environment. A sustainable competitive advantage remains the key consideration in our investments.

Davis International Fund, valued at a P/E multiple of 6.9x compared to the MSCI ACWI ex US at 13.9x, is at a 50% discount to the international index. Given the high quality and durability of our businesses, such a dramatic valuation discount bodes well for future returns. Such a wide discount is akin to starting a 100-yard race at the 50-yard line. One still needs to train and avoid stumbling but it is clearly a considerable advantage.

The recent normalization of interest rates after such a long period of near-zero rates was the biggest shift in the investment landscape in decades. Similarly, the introduction of a useful, cost-effective and easy-to-use generative AI was one of the biggest technological breakthroughs ever. We believe that both of these monumental shifts are net positives for our portfolio of companies. Our mantra that valuation matters rings especially true when capital has a cost. The market has not completely adjusted to the new reality as the S&P 500 Index is still trading at 21x price/earnings but looking at the “S&P 493” (500 less the seven largest tech stocks) trading at more reasonable valuations, one can see that the adjustment is underway. With Davis International Fund at a massive 68% discount to the S&P 500 and at a 50% discount to the MSCI ACWI ex US, the odds are tilted in favor of future outperformance. Our focus on sustainable competitive advantages means that our companies have the scale, technological leadership and experience to widen the lead they already possess, and take advantage of new developments such as AI to deepen their competitive edge.

We understand that in uncertain times such as these, it is more important than ever to be able to entrust your savings to an experienced and reliable investment manager with a strong long-term record. During the 50 years since our firm’s founding, the Davis Investment Discipline has demonstrated an ability to generate above-average returns based on in-depth fundamental research and analysis, a long-term investment horizon and a strong value discipline. While times have changed, these fundamental principles are timeless and proven. We thank you for your continued trust and interest in Davis International Fund.

Source: Robert J. Shiller (Yale University); Federal Reserve Board and Federal Reserve economic data.

The Attractive Growth and Undervalued reference in this material relates to underlying characteristics of the portfolio holdings. There is no guarantee

that the Fund’s performance will be positive as equity markets are volatile and an investor may lose money. Past performance is not a guarantee of future returns. Five-year EPS Growth Rate (5-year EPS) is the average annualized earnings per share growth for a company over the past 5 years. The values shown are the weighted average of the 5-year EPS of the stocks in the Fund or Index. Approximately 14.72% of the assets of the Fund are not accounted for in the calculation of 5-year EPS as relevant information on certain companies is not available to the Fund’s data provider. Forward Price/Earnings (Forward P/E) Ratio is a stock’s price at the date indicated divided by the company’s forecasted earnings for the following 12 months based on estimates provided by the Fund’s data provider. These values for both the Fund and the Index are the weighted average of the stocks in the portfolio or Index.

Private Equity Group (PAG) (Chinese investment bank) report, page 2.

Will China Continue to Grow? by Weijian Shan, 11/14/23, page 4.

Deep learning models can recognize complex patterns in pictures, text, sounds, and other data to produce accurate insights and predictions. https://aws.amazon.com/what-is/deep-learning/#

This material is authorized for use by existing shareholders. A current Davis International Fund prospectus must accompany or precede this material if it is distributed to prospective shareholders. You should carefully consider the Fund’s investment objective, risks, charges, and expenses before investing. Read the prospectus carefully before you invest or send money.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact.

Davis Advisors is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy and approach. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this material. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate.

Objective and Risks. The investment objective of Davis International Fund is long-term growth of capital. There can be no assurance that the Fund will achieve its objective. Some important risks of an investment in the Fund are: stock market risk: stock markets have periods of rising prices and periods of falling prices, including sharp declines; common stock risk: an adverse event may have a negative impact on a company and could result in a decline in the price of its common stock; foreign country risk: foreign companies may be subject to greater risk as foreign economies may not be as strong or diversified; China risk – generally: investment in Chinese securities may subject the Fund to risks that are specific to China including, but not limited to, general development, level of government involvement, wealth distribution, and structure; headline risk: the Fund may invest in a company when the company becomes the center of controversy. The company’s stock may never recover or may become worthless; depositary receipts risk: depositary receipts involve higher expenses and may trade at a discount (or premium) to the underlying security; foreign currency risk: the change in value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency; exposure to industry or sector risk: significant exposure to a particular industry or sector may cause the Fund to be more impacted by risks relating to and developments affecting the industry or sector; emerging market risk: securities of issuers in emerging and developing markets may present risks not found in more mature markets. As of 3/31/24, the Fund had approximately 44.5% of net assets invested in emerging markets; large-capitalization companies risk: companies with $10 billion or more in market capitalization generally experience slower rates of growth in earnings per share than do mid- and small-capitalization companies; manager risk: poor security selection may cause the Fund to underperform relevant benchmarks; fees and expenses risk: the Fund may not earn enough through income and capital appreciation to offset the operating expenses of the Fund; and mid- and small-capitalization companies risk: companies with less than $10 billion in market capitalization typically have more limited product lines, markets and financial resources than larger companies, and may trade less frequently and in more limited volume. See the prospectus for a complete description of the principal risks.

The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. As of 3/31/24, the top ten holdings of Davis International Fund were: Danske Bank, 8.74%; Samsung Electronics, 8.53%; DBS Group Holdings, 7.97%; Meituan, 6.72%; Julius Baer Group, 5.68%; Prosus, 5.45%; Naspers, 5.36%; Teck Resources, 4.97%; Ping An Insurance Group, 4.51%; Tokyo Electron, 4.46%.

Davis Funds has adopted a Portfolio Holdings Disclosure policy that governs the release of non-public portfolio holding information. This policy is described in the statement of additional information. Holding percentages are subject to change. Visit davisfunds.com or call 800-279-0279 for the most current public portfolio holdings information.

The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (MSCI) and S&P Global (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaim all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of such damages.

We gather our index data from a combination of reputable sources, including, but not limited to, Lipper, Wilshire and index websites.

The MSCI ACWI (All Country World Index) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets throughout the world. The index includes reinvestment of dividends, net foreign withholding taxes. Investments cannot be made directly in an index. The S&P 500 Index is an unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The index is adjusted for dividends, weighted towards stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. Investments cannot be made directly in an index.

After 4/30/24, this material must be accompanied by a supplement containing performance data for the most recent quarter end.

Item #4760 12/23 Davis Distributors, LLC, 2949 East Elvira Road, Suite 101, Tucson, AZ 85756, 800-279-0279, davisfunds.com

International Fund

Annual Review 2024

Managers